Nieman Foundation at Harvard

Newspaper companies can be opaque to outside observers. Many of them remain in private hands, unobligated to share any numbers that might make them look bad. Others are wrapped up into giant chains who report things like digital subscriptions or advertising revenue only in lump sums. (When one company owns more than 300 local news properties across two continents, it can be hard to suss out anything granular.) And even then, publicly traded newspaper companies generally only report numbers in quarterly chunks, when the start and end of a three-month period can feel like different universes.

But we do have an interesting set of data points that can give us a more nuanced perspective of what it’s like to run an American newspaper company in 2020. And we have the bankruptcy of the nation’s No. 2 chain, McClatchy, to thank for it.

First, a brief catch-up for those who haven’t been following. McClatchy, which owns 30 newspapers in markets like Miami, Charlotte, and Kansas City, has been living under a debt deadweight for more than a decade, having bought a bigger chain, Knight Ridder, at what turned out to be the industry’s peak in 2006. After years of budget cuts — while still retaining its reputation as a high-quality chain — McClatchy finally declared bankruptcy in February.

When a company files for bankruptcy, it is generally required to periodically report on its financial condition, so that the court and the company’s creditors can have some insight into what shape it’s in. These monthly operating reports are “designed to give interested parties information about the debtor’s business operations in order for them to monitor the likelihood of successful reorganization.”

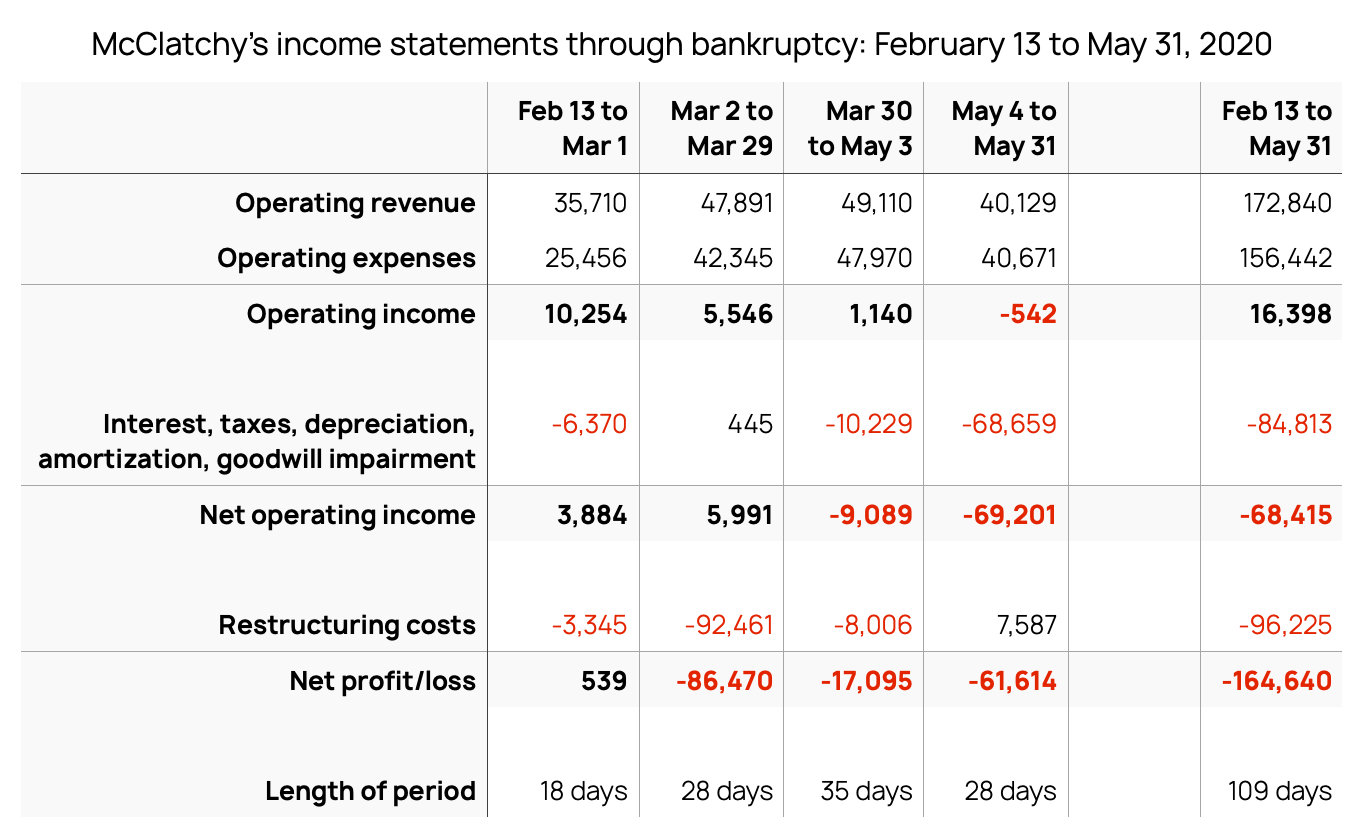

McClatchy has filed four monthly operating reports during its bankruptcy, covering February 13 to March 1, March 2 to March 29, March 30 to May 3, and May 4 to 31. (The budget numbers are on page 5 of each of these PDFs.) That span of time happens to be when the coronavirus hit the United States and ripped up much of the newspaper industry’s ad revenue — so these reports give some insight into the virus’ impact.

I went through and pulled all the numbers together into a table where you can see the changes over time. (All dollar amounts here are in thousands.)

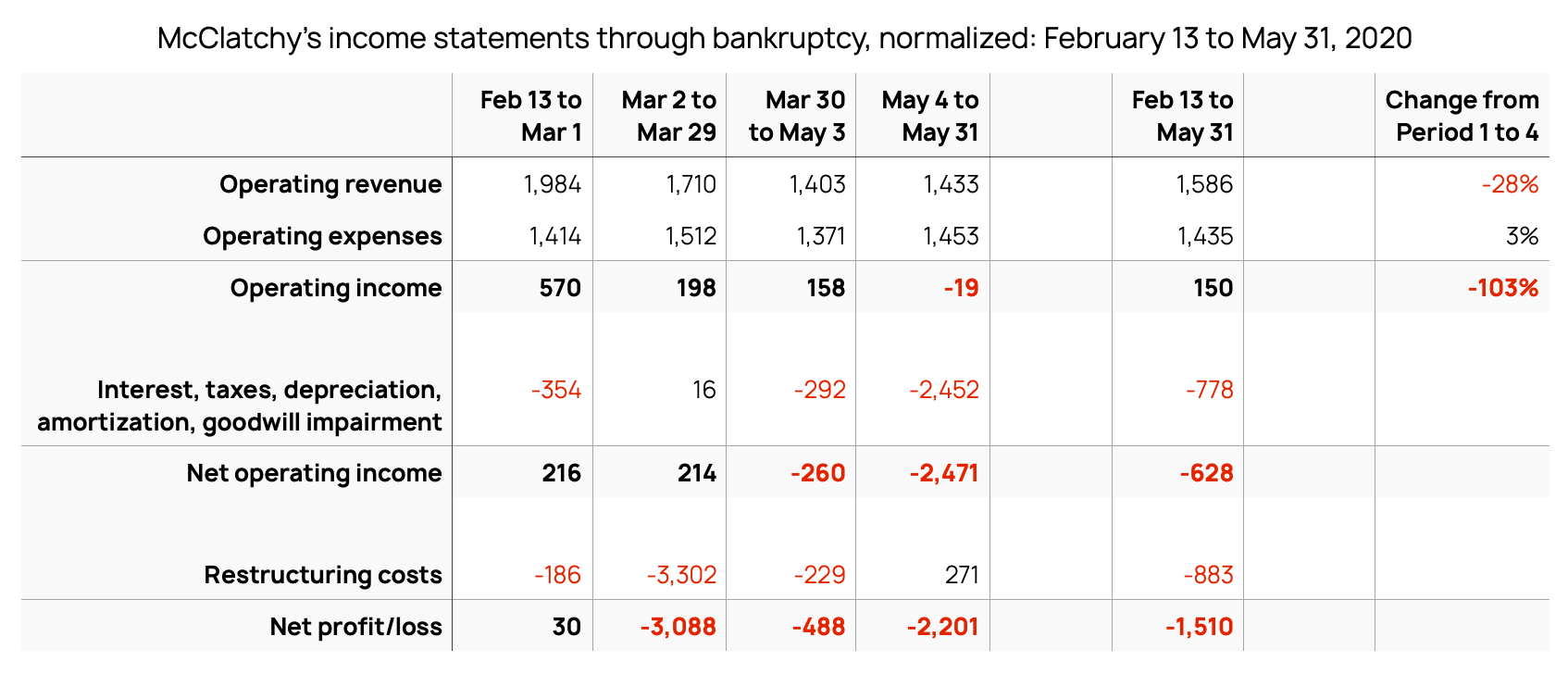

There’s one complicating issue, though. While these are called “monthly” operating reports, you’ll notice that they don’t actually line up to months. They don’t even cover the same lengths of time: 18, 28, 35, and 28 days. So to normalize that, here’s another chart that instead reduces each period down to per-day averages. That allows comparisons that show real trends. Here’s that table:

Let’s walk through it.

At the top, we’ve got the four time periods in question as well as a summary column that combines all four.

Start with the first column, February 13 to March 1. For broader news industry purposes, the important numbers are the top three: operating revenue, operating expenses, and operating income. These measure the core profitability of McClatchy’s operations — EBITDA (earnings before interest, taxes, depreciation, and amortization).

In that February period, pre-Covid impact, McClatchy was averaging daily revenue of $1,984,000 against average daily expenses of $1,414,000. That’s not bad — a healthy margin before taking into account the ITDA in EBITDA. McClatchy had an operating profit in that 18-day span of $10.254 million — also not bad. (Indeed, in Q3 2019, the last quarterly earnings it filed before bankruptcy, McClatchy reported its first increase in EBITDA in eight years.)

Of course, you can’t just wish the ITDA in EBITDA away. Interest, taxes, depreciation, and amortization reduced that $10.254 million to $3.884 million. But still, extrapolate that over an entire year and it’s a profit of $78.7 million.

The final set of dollar figures in that column account for the fact that McClatchy was newly bankrupt in February, and filing for bankruptcy costs money. The $3.345 million spent on “restructuring costs” — lawyers, plus other “professional fees” — ate up most of the revenue that remained, leaving a profit of $539,000.

It’s not a terrible start. But in the next three columns, you can see how the virus did McClatchy — and the entire news business — dirty.

McClatchy’s average daily operating revenue across these four periods dropped from $1.984 million to $1.710 million to $1.403 million to $1.433 million between February and the end of May. That’s a decline of 28 percent.

These monthly operating reports don’t break down revenue sources. But as of Q3 2019, McClatchy made 46.8 percent of its revenue from the audience (print and digital subscriptions), 45.8 percent from advertising, and 7.3 percent from everything else. During Covid, McClatchy, like other news companies, has seen increases in subscriptions, so that piece of the pie is probably up, not down. That means the hit to advertising is really bad — perhaps 40 percent or more.

By late March, publishers could see the scale of the advertising damage and began to make cuts. On April 9, McClatchy announced furloughs for 4.4 percent of its employees, along with executive layoffs and pay cuts — a less severe package of cost reductions than some other companies like Gannett made. But it’s hard to see a clear cost reduction across these four periods; average daily operating expenses were even slightly higher in May ($1.453 million) than they were in late February ($1.414 million).

Add those up and you see the impact on EBITDA: from plus $570,000 a day to minus $19,000 a day.

The lower levels of the chart are mostly of interest to McClatchy and its employees, not particularly indicative of anything larger in the industry.

Two numbers are worth highlighting. First, the catch-all “Interest, taxes, depreciation, amortization, goodwill impairment” sees a huge swing in May, with a loss of $68.6 million. Most of that is actually an income adjustment driven by “the final Impairment of goodwill and other intangible assets for $63.8 million.” It’s an accounting charge.

Second, we have the ballooning “restructuring costs” in the March 2–29 period — $92.4 million. That’s also mostly an accounting matter; $83.1 million of that total is a “write off of debt issuance fees,” plus another $8.6 million in professional fees and $800,000 in lease termination costs.

Wonder how much the lawyers are making? The total cost for professional fees relating to the bankruptcy across this period is $25.4 million. Those fees have been piling up for almost another seven weeks since McClatchy’s last filing, so the total cost will almost certainly top $30 million, perhaps by a significant margin.

Given that Chatham is taking the company private — and that any potential return to the stock market would involve merging into some other consolidator — these may well be the last real financials we ever see from McClatchy.

Combined with previous earnings reports, they show a company that has managed the digital transition better than most; at last public count, it was making nearly half of its ad revenue in digital, and digital subscriptions were up 45 percent year-over-year.

They show a company that was able to be operationally profitable while still doing good journalism.

But they also show a company so laden with 14-year-old debt that it had to enter Chapter 11. A company that is trading 163 years of family stewardship for a hedge fund that also owns the National Enquirer. And a company, like all of its industry peers, that got walloped by a virus it had no control over.